Effective January 1, 2023, there are two new excise tax rates on natural gasoline that may apply to ethanol producers.

IRA Update

The Inflation Reduction Act of 2022 (IRA) amended the Hazardous Substance Superfund financing rate on domestic crude oil and imported petroleum products. Section 4611.Impostion of Tax under Title 26 Subchapter A – Tax on Petroleum imposes a two-part tax on petroleum with new rates effective January 1, 2023.

The tax rate on domestic crude oil and imported petroleum products is the sum of the Oil Spill Liability Trust Fund financing rate (petroleum oil spill tax rate or OSLT) and the Hazardous Substance Superfund financing rate (petroleum superfund tax rate)(1). It is calculated per barrel of product. The IRS defines a barrel as 42 gallons(2).

- The petroleum oil spill tax rate is $0.09 per barrel ($0.0021 cents per gallon)

- The petroleum superfund tax rate is $0.164 per barrel ($0.0039 cents per gallon) for 2023 (rate is indexed annually for inflation)

Background

These two petroleum taxes are typically imposed on either the refinery receiving the petroleum product or on the importer of the petroleum product, in accordance with IRC section 4611(a). However, if the crude oil or petroleum product is used before it is taxed per 4611(a), then according to section 4611(b), the tax still applies, and the user is liable for the tax.

Natural gasoline is methanol produced from natural gas. According to the IRS, “crude oil includes crude oil condensates and natural gasoline. Petroleum products include crude oil, refined and residual oil, and other liquid hydrocarbon refinery products.”(3)

Natural gasoline is typically produced by fractionation facilities, rather than refineries. The IRS does not consider fractionation facilities to be United States refineries(4). In other words, natural gasoline produced by a fractionation facility is considered taxable crude oil that is never received by a refinery. Therefore, the user of the natural gasoline is liable for these two petroleum taxes.

Implications for Ethanol Producers

Ethanol producers using natural gasoline as a denaturant for fuel ethanol before the natural gasoline has been received by a refinery are liable for paying the OSLT and the petroleum superfund tax.

If an ethanol producer can demonstrate that the natural gasoline it purchases was received by a United States refinery prior to its use as a denaturant for fuel ethanol, then the ethanol producer will not be liable for paying the OSLT nor the petroleum superfund tax.

Tax Filing & Deposits

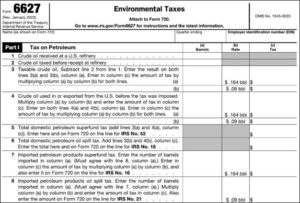

The OSLT and petroleum superfund tax are payable on IRS Form 720 (Excise Taxes) as calculated from worksheet IRS Form 6627 (Environmental Taxes). On Form 6627, the quantity of barrels of natural gasoline used is entered in Part 1 on both lines 4(a) for the petroleum superfund tax and 4(b) for the OSLT. The total tax as calculated from line 4(a) in column (c) is entered on line 5 – this number is entered on Form 720 on the line for IRS No. 53. The total tax as calculated from line 4(b) in column (c) is entered on line 6 – this is entered on Form 720 on the line for IRS No. 18. The IRS released an updated version of Form 720 in March 2023 that includes IRS No. 53 for the petroleum superfund tax.

Deposits for the OSLT and petroleum superfund are due beginning in January 2023. The deposits are due semi-monthly and follow the existing excise tax deposit schedule. Refer to IRS Publication 509 for the current year’s deposit schedule (5).

Assistance for Ethanol Producers

Our team of tax experts is ready to assist ethanol producers in understanding their excise tax responsibilities as it pertains to the denaturant they purchase. Our tax and advisory services include helping companies calculate excise tax liabilities, remit deposits, and file quarterly 720 returns. We also provide tax training and assist companies in creating internal policies and procedures for tax compliance. Reach out today to speak with one of our experts to learn how we can best meet your company’s needs.

1 IRC Title 26 Section 4611 Imposition of Tax https://www.law.cornell.edu/uscode/text/26/4611

2 IRC Title 26 Section 4612 Definitions and special rules https://www.law.cornell.edu/uscode/text/26/4612#a_8

3 Publication 510 (07/2021), Excise Taxes https://www.irs.gov/publications/p510

4 Internal Revenue Bulletin No. 1998-11 https://www.irs.gov/pub/irs-irbs/irb98-11.pdf

5 IRS Publication 509 Tax Calendars for Use in 2023 https://www.irs.gov/pub/irs-pdf/p509.pdf